Platforms: Aave (potentially expanding to Euler and/or Morpho later)

Underlying assets: Stablecoins (e.g. USDT, USDC, USDe) and Principal Tokens (PT-USDe and PT-sUSDe) for now.

What is Looping?

Looping strategies involve borrowing against collateral and reusing the borrowed funds to purchase more of the same collateral, repeating this cycle multiple times. The result is a leveraged position that amplifies both yield and risk.

For example, you could borrow USDC against 7% APY and buy PTs which yield 10% APY. You’d then borrow more USDC using the bought PTs as collateral, and repeat the loop. This way you capitalise on the interest rate spread with leverage.

For Noon, looping is attractive because it transforms modest base yields into scalable returns (15–30% APY), while still using liquid, trustworthy collateral types. However, it introduces liquidation risk and operational complexity, which must be carefully managed.

Read our full Looping Primer for a detailed walkthrough of how Looping works, the mechanics, examples, risks, and more.

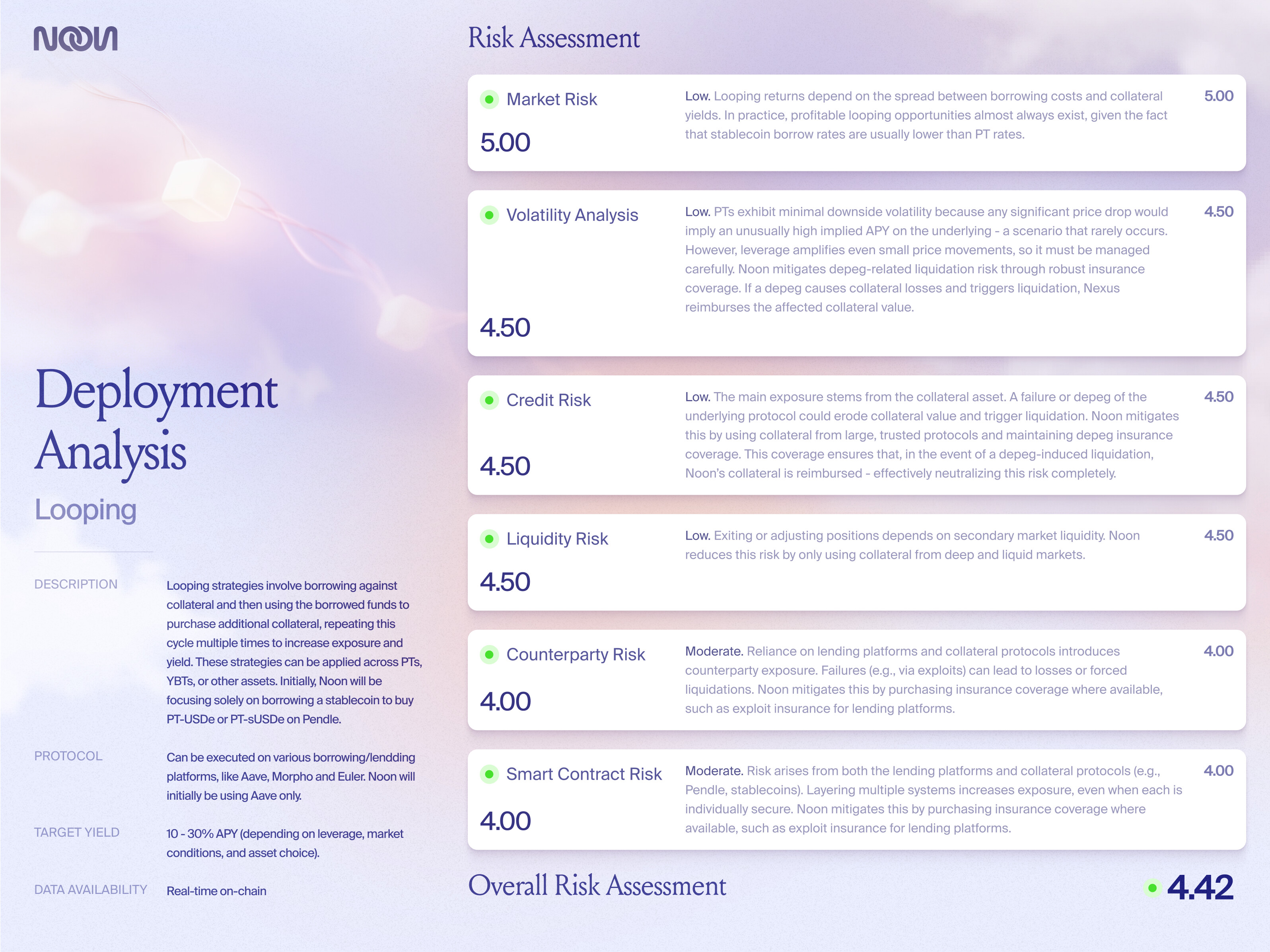

Noon Risk Assessment: Summary

Noon Deployment Analysis – Looping

Market Risk

Low — Looping returns depend on the spread between borrowing costs and collateral yields. In practice, profitable looping opportunities almost always exist, given the fact that stablecoin borrow rates are usually lower than PT rates.

Volatility Risk

Low — PTs exhibit minimal downside volatility because any significant price drop would imply an unusually high implied APY on the underlying - a scenario that rarely occurs. However, leverage amplifies even small price movements, so it must be managed carefully. Noon mitigates depeg-related liquidation risk through insurance coverage: if a depeg causes collateral losses and triggers liquidation, Noon’s insurance coverage would reimburse Noon for the affected collateral value.

Credit Risk

Low — The main exposure stems from the collateral asset. A failure or depeg of the underlying protocol could erode collateral value and trigger liquidation. Noon mitigates this by using collateral from large, trusted protocols and maintaining depeg insurance coverage. This coverage ensures that, in the event of a depeg-induced liquidation, Noon’s collateral is reimbursed - effectively neutralising this risk completely.

Liquidity Risk

Low — Exiting or adjusting positions depends on secondary market liquidity. Noon reduces this risk by only using collateral from deep and liquid markets.

Counterparty Risk

Moderate — Reliance on lending platforms and collateral protocols introduces counterparty exposure. Failures (e.g., via exploits) can lead to losses or forced liquidations. Noon mitigates this by purchasing insurance coverage where available, such as exploit insurance for lending platforms.

Smart Contract Risk

Moderate — Risk arises from both the lending platforms and collateral protocols (e.g., Pendle, stablecoins). Layering multiple systems increases exposure, even when each is individually secure. Noon mitigates this by purchasing insurance coverage where available, such as exploit insurance for lending platforms.

Our analysts’ recommendation

We’ve completed our initial review and now invite community feedback on whether Noon should add Looping Strategies to its permitted deployment basket.

Recommendation: Proceed — with strict leverage and asset selection rules. Why?

-

Attractive yields: Looping can consistently deliver higher APYs than simple lending or vanilla PT exposure.

-

Risk-aware fit: While looping carries liquidation risk, careful asset selection, leverage controls and coverage through Nexus can make it a safe and scalable strategy.

Risk controls we will enforce:

-

Leverage caps: Maximum leverage limits to reduce liquidation risk.

-

Collateral selection: Only PT-USDe and PT-sUSDe for now.

-

Position sizing: Pool- and protocol-level caps to avoid concentration.

-

Monitoring: Automated health-factor alerts and stress tests to flag liquidation risk early.

-

Insurance: Coverage against depeg-induced liquidations through Nexus.

Together, these measures balance attractive returns with controlled risk.

Internal Looping Exposure

Noon will never loop using its own tokens (USN/sUSN) as collateral. Doing so would effectively amount to “self-dealing”, which undermines collateral integrity. Our looping strategy will focus exclusively on external assets.

Let’s Open the Discussion, Noon Community:

We propose adding Looping to Noon’s basket of permitted deployment strategies, subject to the constraints above. We invite discussion in this thread for the next 10 days. After that, we’ll open an official vote for all $sNOON holders to include or exclude Looping from our permitted strategies.

You don’t need to answer every angle — just share what feels most important to you. For example:

- Do you support adding Looping under these conditions?

- Any concerns we should keep in mind (e.g., liquidity depth, underlying asset risk)?

- Anything we might be missing?

Drop your comments below ![]()